Warsh takes office tomorrow! What will happen to the US stock market after the change of Fed chair? Historical data reveals this surprising signal.

According to Xinhua News Agency, Kevin Warsh will be sworn in as Chairman of the Federal Reserve on May 22 local time. US President Trump will hold an inauguration ceremony for Warsh at the White House.

Who is the new Federal Reserve Chairman, Warsh? What are his specific policies and propositions?

Will the appointment of a new Federal Reserve Chairman be a boon or a bane to the ever-rising US stock market? Data shows that the average maximum drawdown in US stocks within six months of a change in Federal Reserve Chairman reaches 16% . How should investors respond? This article will provide investors with insights into the new Federal Reserve Chairman.

Who is Kevin Walsh? He's considered one of Trump's "insiders"! His father-in-law is a longtime friend of Trump.

Kevin Walsh was born in 1970 and is currently 55 years old. He holds a Juris Doctor degree. His educational background is outstanding: he graduated from Stanford University in 1992 with a Bachelor of Arts degree in Public Policy, majoring in Economics and Political Science; and he received his Juris Doctor degree from Harvard University in 1995.

Walsh has an impressive resume, spanning politics, business, and academia, earning him the title of a "triple threat."

- In politics, Warsh served as a special assistant to the president on economic policy in the Bush administration; at the age of 35, he became the youngest governor in the history of the Federal Reserve ; and in 2008, he had experience communicating with Wall Street and was regarded as a person who could "talk to the market" .

- In the business world, Walsh has a Wall Street background, having served as Vice President and Executive Director in the M&A department of Morgan Stanley, and is considered to "understand the market and understand transactions" .

- On the academic front, Walsh is currently a Shepherd Family Distinguished Visiting Fellow at the Hoover Institution at Stanford University, a truly illustrious career.

It is worth noting that Warsh had a close relationship with Trump and was widely considered one of Trump's "insiders." Trump repeatedly praised Warsh publicly for his "outstanding image" and "competent ability."

Most importantly, Walsh's wife is Estée Lauder, the heiress to the Estée Lauder fortune, and his father-in-law, Ronald Lauder, is a longtime friend of Trump and heir to the Estée Lauder Companies. According to foreign media reports, Lauder and Trump were classmates and have known each other for over 60 years. Trump's obsession with Greenland stems from Lauder's "suggestion."

Warsh's policy proposals include: promoting a combination of interest rate cuts and balance sheet reduction, with plans to implement disruptive reforms!

Kevin Warsh was confirmed by the U.S. Senate (54 votes in favor, 45 against) to succeed Jerome Powell as Chairman of the Federal Reserve. As a "system reformer," Warsh proposed a comprehensive reform blueprint centered on "interest rate cuts, balance sheet reduction, regulatory deregulation, and institutional reform," and his policy framework is mainly reflected in the following dimensions:

I. Criticizing Powell's over-reliance on lagging data! Warsh is determined to reconstruct inflation measurement indicators.

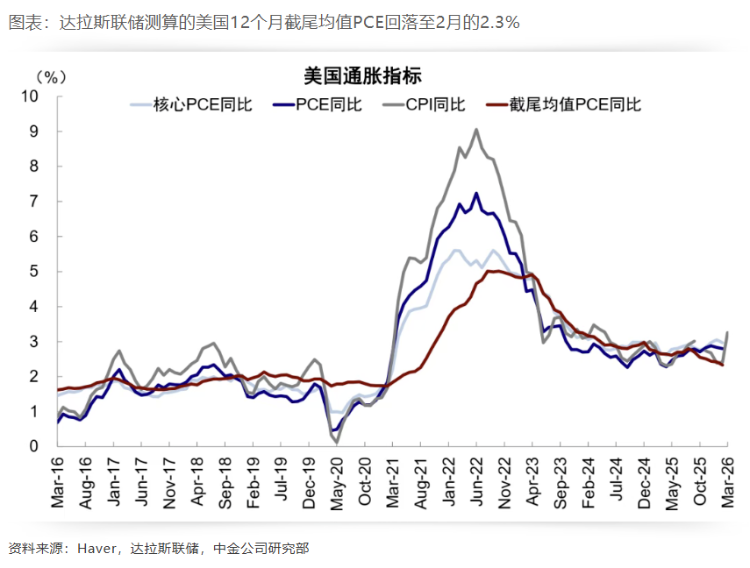

Warsh argues that the Federal Reserve's over-reliance on the "core PCE," which excludes food and energy prices, as a measure of inflation could lead to policy misjudgments. He advocates using the "truncated mean method" to calculate the inflation rate, which removes extreme values from price fluctuations, thereby more accurately reflecting the impact of general price changes on the economy.

According to Bank of America data, the 12-month cutoff inflation gauge calculated using the Warsh method has a mean of 2.3% and a median of 2.8%, while the core PCE for the same period was 3%. This difference provides a theoretical basis for Warsh's advocacy of interest rate cuts—he believes that the current inflation trend is actually more moderate than the Federal Reserve considers. In other words, referring to the cutoff mean gauge would give the Federal Reserve more room to maneuver in cutting interest rates.

Furthermore, Warsh pointed out that the productivity boom driven by artificial intelligence constitutes a significant anti-inflationary force, which the Federal Reserve has failed to fully recognize. He advocates using AI to improve productivity and suppress long-term inflation, supporting faster and earlier interest rate cuts, which contradicts Powell's "anti-inflation priority" stance.

Second, the implementation of a parallel policy of "interest rate cuts + balance sheet reduction" faces severe challenges.

The "interest rate cuts + balance sheet reduction" policy is Warsh's most controversial policy proposition. He emphasizes that the Federal Reserve will only have the policy space to cut interest rates when the balance sheet returns to a reasonable size. The market expects him to push for 1-3 rate cuts (25-50 basis points) after taking office . At the same time, Warsh has long criticized the normalization of quantitative easing, believing that the Fed's balance sheet of approximately $7.5 trillion is "dangerously bloated," causing capital mismatch and distorting financial markets. He plans to more proactively reduce the balance sheet, expecting the reduction to exceed $1 trillion in the next two years.

This combination faces an inherent contradiction: interest rate cuts, which are considered an easing measure, will increase liquidity, while balance sheet reduction, which is considered a tightening measure, may trigger a sell-off of US Treasuries and push up US Treasury yields. There is a policy hedging effect between the two.

It's worth noting that just before the swearing-in ceremony, Warsh's long-advocated interest rate cut strategy faced a serious test! Over the past week, the US Treasury market has been undergoing a repricing process—the 30-year Treasury yield briefly broke through 5%, reaching its highest level since before the 2007 global financial crisis; while the 2-year yield, most sensitive to policy, even surpassed the upper limit of the Fed's policy rate target range of 3.50%-3.75%, rising above 4%. This is equivalent to the bond market having already "raised interest rates" for Warsh , making his interest rate cut + balance sheet reduction strategy highly questionable. However, Trump has recently clearly "softened his stance," stating that Warsh can "determine interest rates as he sees fit."

Third, change the Federal Reserve's communication mechanism and weaken "forward guidance".

Warsh argues that the Federal Reserve "talks too much," which actually reduces policy flexibility. He believes the Fed's "excessive communication" undermines the authority of its policy, and when the market becomes accustomed to the Fed "spoiling" its policy path in advance, it will become overly reliant on official statements. If actual data deviates from expectations, the market will experience severe volatility. Therefore, he advocates:

- Abolish dot plots: Criticisms suggest that dot plots and other similar tools are overly transparent and interfere with market judgment.

- Reduce the frequency of press conferences : Minimize unnecessary expectation management

- Reforming the communication mechanism : enabling the Federal Reserve to speak with a more unified voice.

Warsh favored making monetary policy signals simpler and more predictable to avoid excessive market reliance on the Federal Reserve. However, this strategy has also sparked considerable controversy. Colin Anderson, a professor at the State University of New York, believes that "without open and transparent official communication, the market can only interpret policy moves on its own. This creates many hidden dangers, the biggest of which is exacerbating market uncertainty ."

Will US stocks continue to rise after Warsh takes office? Historical data suggests a pullback is highly probable!

Recently, US stock indices have continued to rise, with the Dow Jones Industrial Average briefly breaking through the 50,000-point mark, and the Nasdaq and S&P 500 rising by more than 10% and 7% respectively this year. Looking at the annual chart, the US stock market is currently in an unprecedented bull market. Will the appointment of new Federal Reserve Chairman Warsh interrupt this trend?

According to Wind data, historically , after each Federal Reserve Chairman takes office, the US stock market has experienced varying degrees of pullback for a period of time.

In particular, after Greenspan took office in 1987, the US stock market experienced a rare stock market crash. The Dow Jones Industrial Average plummeted 22.6% in a single day without any obvious negative news, marking the largest single-day drop since 1941, and was known as "Black Monday".

Within 10 months of Powell taking office in 2018, the S&P 500 index had fallen by nearly 20%. Furthermore, previous Federal Reserve chairs, including Volcker, Bernanke, and Yellen, all experienced stock market corrections in the months following their appointments.

In its research report, Barclays concluded that since 1930, the average maximum drawdown of the S&P 500 index in the first, third, and sixth months after a new Federal Reserve chairman takes office has been 5%, 12%, and 16%, respectively , all exceeding the decline of the S&P 500 index between typical peaks and troughs in any randomly selected year.

Why did US stocks generally decline in the short term after a change of Federal Reserve chair? Analysts believe this is mainly due to the uncertainty surrounding the monetary policy path, leading to a restructuring of expectations , and risk aversion caused by market unfamiliarity with the successor's policy style . Chuancai Securities points out that a change of leadership implies potential adjustments to monetary policy direction and the pace of monetary easing, changes in global liquidity expectations, and market speculation on changes in interest rates and balance sheet reduction policies, thus triggering valuation fluctuations. DBS Bank believes that the so-called short-term decline following a change of leadership is mostly a manifestation of investors' concerns about the uncertainty of the successor's monetary policy . Unless the successor explicitly states before taking office that they will introduce monetary policies unfavorable to the stock market, in the short term, investors are simply experiencing some risk aversion due to a lack of complete understanding of the new chair's specific policies.

How should investors respond? These directions can serve as a reference!

For investors concerned that the US stock market might repeat its previous decline after the change of leadership at the Federal Reserve, they might consider investing in short-selling ETFs, such as:

- The 3x short Nasdaq 100 ETF ( $SQQQ ) shorts the Nasdaq 100 index. When the Nasdaq retraces, this ETF will rebound at three times the rate. It is suitable for those who are bearish on US technology stocks (Tesla, Nvidia, Apple, etc.).

- The ETF, which leverages a 3x short position in the Dow Jones Industrial Average ($SDOW) , is betting on a decline in traditional industrial and financial stocks.

- A 3x leveraged short position in the S&P 500 index ($SPXU) , which covers 500 large U.S. companies.

- Double-leverage shorting of the Russell 2000 index $TWM , focusing on shorting US small and mid-cap stocks, resulting in higher volatility.

It's worth noting that both $SOXS and $SQQQ , these leveraged inverse ETFs, use daily compounding resets. When the market fluctuates repeatedly and fails to break out of a one-sided downward trend, even if the semiconductor price ultimately remains unchanged, these ETFs will continue to lose money due to leverage decay. If you don't want to bear the leverage decay, the most direct method is to do what short seller Michael Burry did: directly buy forward put options on $SOXX , or directly short $SOXX. .

Furthermore, historical data shows that when US stocks decline, healthcare, consumer staples, and utilities are generally considered defensive sectors, potentially offering better protection against market downturns. Relevant ETFs to consider include $XLV , $XLP , and $XLU .

type | code | introduce |

Leveraged short ETFs | Triple short position in Nasdaq ETF $SQQQ | Shorting the Nasdaq 100 is suitable for those who are bearish on US tech stocks. |

Triple short position in the Dow Jones Industrial Average ETF $SDOW | There is a bias towards betting on a decline in traditional industrial and financial stocks. | |

Triple short S&P 500 ETF $SPXU | It covers 500 large US companies and shorts the overall stock market. | |

Double short the Russell 2000 ETF $TWM | Focus on shorting US small and mid-cap stocks, which are more volatile. | |

Three times short the semiconductor index $SOXS | Shorting semiconductor stocks such as Nvidia, Micron, SanDisk, and Intel. | |

Triple short position in US small-cap ETF $TZA | It hedges against the decline in small-cap stocks, has high trading volume, and high liquidity. | |

Traditional defensive sector ETF | Healthcare ETF $XLV | Those who heavily invest in companies like Eli Lilly and Johnson & Johnson are generally considered to have strong defensive characteristics. |

Consumer Staples ETF $XLP | Holding consumer stocks such as Walmart and Procter & Gamble makes them less affected by economic cycles. | |

Utilities ETF $XLU | It covers a range of energy and power stocks, which are less affected by economic cycles. | |

Vanguard Values ETF $VTV | Investing heavily in undervalued, high-dividend value stocks may yield excess returns during a bear market. |

So, as a savvy investor, what are your thoughts on the performance of the US stock market since Warsh took office? Feel free to leave a comment below!

Risk Warning: Investing involves risks. Securities prices can rise or fall, and may even become worthless. Investing does not guarantee profits and may even result in losses. Past performance is not indicative of future results. Before making any investment decisions, investors must assess their own financial situation, investment objectives, experience, risk tolerance, and understand the nature and risks of the relevant products. For details regarding the nature and risks of individual investment products, please carefully read the relevant sales documents for more information. If you have any questions, you should seek independent professional advice.