Keywords of HK IPO Allotment

Are you curious about the allotment mechanism of HK IPOs? Let’s take a look at some terms that you might come across when applying for HK IPOs and checking the allotment results. They may sound unfamiliar right now, but you’ll gain a better understanding of them in no time.

International placement (Group A) and public offering (Group B):

The allotment of new Hong Kong shares is divided into two parts: international placement (Group A) and public offering (Group B). 90% of new shares are directly distributed in international placement (Group A), which mostly consists of professional investors, including large institutional investors and individual investors with strong capital.

International placement and public offering provide two ways of alloting new shares. The relationship between the two is like wholesale and retail. One buys more, and the other buys less and more scatteredly. International placement is aimed at investors with strong global strength, big subscription funds and can be purchased in large quantities. Typically, the threshold that separates international placement from public offering is HKD 5 million.

A public offering is common for retail investors, and the amount of funds is relatively small. With M+ Global, you can subscribe to IPOs through public offering of new shares.

Since the subscription funds of international placement far exceed those of public offering, the number of shares allotted to international placement is also larger - with a general ratio of 9:1. As mentioned, the number of shares for international allotment accounts for 90%, while public allotment accounts for 10%. So as an example, in 2019, $Alibaba-SW hk09988$ went public in Hong Kong and issued a total of 500 million common shares - 90% of which were for international placement, and 10% for public placement. This resulted in 450 million for the former and 50 million for the latter.

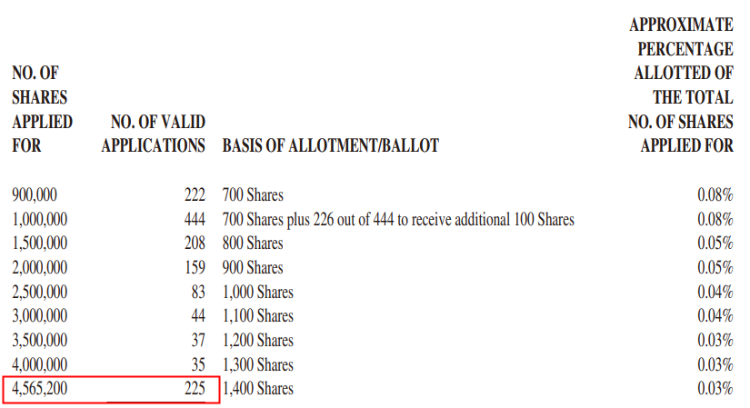

What is a top mallet?

The biggest individual investor of a public offering (Group B) with the most lots is called the "top mallet”. For instance, $Kuaishou hk01024$ initially issued 9,130,500 shares available for public offering, with 225 applicants subscribing to 4,565,200 shares per person. These applicants who subscribed to the most number of shares in Group B are therefore called “top mallet”, and are allotted 1,400 shares (14 lots) per person.

What is the claw-back mechanism?

The clawback mechanism is a provision to adjust the number of new shares issued. In order to ensure the success of the issuance and fair trading, the number of shares issued under different issuance methods is first manually set (10% for the public, for example). Then the number of offerings is adjusted between public offerings and international placements according to the subscription results and rules followed.

The public offering (Group B) of most newly listed shares accounts for 10% of the total. If the oversubscription by retail investors is within 15 times, no clawback will be made. The ratio of public offering (Group B) and international placement (Group A) remains 1:9.

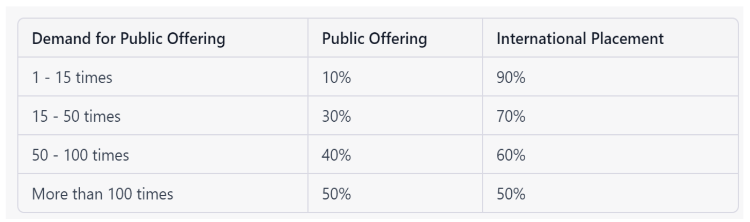

The following are the rules of the clawback mechanism by HKEX:

a. An initial allotment of 10% of the shares offered in the IPO;

b. a clawback mechanism that increases the number of shares to 30% when the total demand for shares in Group B is 15 times, but less than 50 times the initial allotment;

c. a clawback mechanism that increases the number of shares to 40% when the total demand for shares in Group B is 50 times, but less than 100 times the initial allotment;

d. a clawback mechanism that increases the number of shares to 50% when the total demand for shares in Group B is 100 times, or more than the initial allotment.

In 2019, the public offering of $EuroEyes hk01846$ was oversubscribed by 42.72 times. After the clawback, the public offering accounted for 30% of the final share (rule b. above).

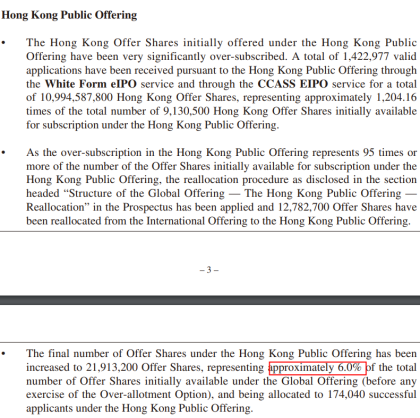

However, not all companies follow that rule specifically. Renowned companies like Alibaba and Kuaishou have their own calculation methods. We know that $Kuaishou hk01024$ was one of the hottest IPOs in 2021 with an oversubscription rate of 95 times for its public offering and 39 times for international placement. The final allotment ratio to the public was only 6% of the total shares.

Take note that the clawback mechanism is essentially a game mechanism between listed companies and investors. When the market is good, it often triggers a double-full amount of clawback, which is easy to make a lot of money. But if the market is cold, the clawback mechanism will also fail and lose its value.